Whether or not it’s refining what you are promoting mannequin, mastering new applied sciences, or discovering methods to capitalize on the following market surge, Inman Join New York will put together you to take daring steps ahead. The Subsequent Chapter is about to start. Be a part of it. Be a part of us and hundreds of actual property leaders Jan. 22-24, 2025.

Individuals could also be rooting for house costs and mortgage charges to return crashing again to Earth in 2025, however affordability is extra prone to return step by step if the decelerating financial system pulls off a smooth touchdown, forecasters say.

Assuming financial development retains chugging alongside at a wholesome tempo and unemployment stays low, mortgage charges would possibly come down a hair, however aren’t anticipated to drop under 6 p.c till 2026 or later.

TAKE THE INMAN INTEL INDEX SURVEY FOR DECEMBER

Odeta Kushi

Residence worth appreciation in lots of markets is anticipated to sluggish, however not reverse, as hundreds of thousands of householders proceed to really feel locked in to the low price on their current mortgage, stated Odeta Kushi, deputy chief economist at First American Monetary Corp.

“Only so much supply can come online because there’s still a lot of existing homeowners that are rate-locked into their home,” Kushi stated. “More than 80 percent of existing homeowners have a rate below 6 percent, so they’re not going to be financially unlocked anytime soon.”

Residence worth appreciation decelerating

Supply: Fannie Mae Housing Forecast, December 2024.

“I do anticipate nationally that house prices will stay positive, but [appreciation will slow to] the low single digits,” Kushi stated.

That’s in step with the most recent forecast from economists at Fannie Mae, who see house worth appreciation decelerating from round 6.4 p.c as we speak to three.6 p.c by the fourth quarter of 2025 and 1.7 p.c by This fall 2026.

Mark Palim

“Underneath that, there may well be some markets that post very small negative (price) declines,” Fannie Mae Chief Economist Mark Palim instructed Inman. “The dynamics we’re seeing in the housing market are a substantial regional variation because of the relative importance of new homes in different markets.”

The place assist would possibly come from

Forecasters say there are two components that might work in favor of homebuyers within the New 12 months:

- With existing-home costs hitting new all-time highs in 2024, homebuilders shall be incentivized to finish new homes as quick as they will.

- Incomes might develop quicker than house costs for the primary time in additional than a decade.

“While mortgage rates will continue to present an affordability challenge, softening home price appreciation in 2025 could allow for nominal wage growth to exceed home price growth for the first time since 2011, helping to start a gradual improvement in homebuyer affordability conditions,” Fannie Mae economists stated in commentary accompanying their newest forecast.

After rising by about 4 p.c this 12 months, Fannie Mae economists suppose new-home gross sales might proceed to be a vivid spot subsequent 12 months, forecasting that the phase will develop one other 9 p.c in 2025 to 755,000.

Traditionally, median costs for brand new houses have far exceeded median costs for current houses. However figuring out that affordability is a matter for a lot of homebuyers, builders are constructing smaller houses that might make new houses an possibility for first-time homebuyers in lots of markets.

Since peaking at 2,519 sq. ft in Q1 2015, the median sq. footage of newly accomplished houses has shrunk by 14 p.c, to 2,158 sq. ft in Q3 2024. Over that interval, the value premium between the median-priced new house versus current houses has declined from 28 p.c to 4 p.c.

Kushi stated builders seeking to break floor on extra houses face a variety of challenges, together with laws and labor and materials prices.

Housing begins per 1,000 households, 1920-2023

Housing begins per 1,000 households have been under the pre-pandemic historic common of 18.85 since 2006. Supply: First American evaluation of U.S. Census Bureau and U.S. Division of Housing and City Improvement (HUD) knowledge retrieved from FRED, Federal Reserve Financial institution of St. Louis.

The tempo of new-home development dropped far under the historic trendline throughout the Nice Recession of 2007-09 and has but to totally recuperate.

However builders had 9.5 months of stock on their arms in October, and Kushi expects they’ll proceed to supply incentives like mortgage price buydowns to spice up affordability and gross sales.

“I do think that [builders] have a competitive advantage over the existing-home market and that the new-home market will continue to outperform the existing-home market next year,” Kushi stated.

The mortgage lock-in impact

Inventories of current houses have been constrained by the mortgage “lock-in effect” — the monetary incentive to remain in a house financed by a mortgage with a low price.

Many owners who purchased or refinanced their house at a decrease price throughout the pandemic is likely to be itching to maneuver — or just commerce up or down — however determined to remain put after doing the mathematics.

Think about a home-owner who refinanced an impressive mortgage steadiness of $500,000 on their 3,000-square-foot home in 2021 by taking out a mortgage at 3 p.c with a month-to-month fee of about $2,100.

Downsizing to a 1,500-square foot house with a $350,000 mortgage on the present price of round 6.9 p.c would saddle them with a month-to-month fee of $2,300. A smaller home, a smaller mortgage, and a bigger month-to-month fee: Not a lot of an incentive to make a transfer.

Equally, ICE Mortgage Know-how estimated in April that buying and selling as much as a house price 25 p.c extra would greater than double the month-to-month fee of the common mortgage holder.

As a result of owners in costlier markets quit decrease charges on larger balances, the lock-in impact is considered notably pronounced in costlier California metros like San Jose, Los Angeles, San Diego and San Francisco.

As of mid-2024, the common house owner’s mortgage price was 2.54 p.c decrease than the present market price, a “level of lock-in unprecedented in recent history,” in keeping with researchers at Fannie Mae and Freddie Mac’s federal regulator.

The lock-in impact is estimated to have prevented 1.72 million gross sales over the previous two years, growing house costs by an estimated 7 p.c, the Federal Housing Finance Company concluded in a latest evaluation.

Residence costs hit all-time highs

Whereas rising wages have been a latest driver of inflation, would-be homebuyers have seen their earnings positive aspects greater than worn out by the double whammy of rising house costs and rates of interest. Greater house costs and inflation have additionally pushed up different bills that influence affordability, like taxes and insurance coverage.

After the subprime housing bust and Nice Recession of 2007-2009, it took greater than a decade for house costs to return to their 2006 peaks, in keeping with the S&P CoreLogic Case-Shiller U.S. Nationwide Residence Worth Index.

However house worth appreciation accelerated throughout the pandemic when record-low mortgage charges and the rising reputation of working from house helped gasoline purchaser demand. Over the previous 5 years, that index exhibits house worth appreciation has averaged near 9 p.c a 12 months.

As of September, nationwide house costs had been up 142 p.c from their February 2012 lows and 76 p.c from the 2006 excessive seen throughout the subprime lending growth, in keeping with the S&P CoreLogic Case-Shiller U.S. Nationwide Residence Worth Index.

Though annual house worth appreciation is slowing, the median gross sales worth of current houses climbed above $400,000 in April and hit an all-time excessive of $432,900 (revised) in June, in keeping with knowledge tracked by the Nationwide Affiliation of Realtors (NAR).

With mortgage charges at round 7 p.c, NAR calculated that even homebuyers placing 20 p.c down would want to earn greater than $110,000 a 12 months to qualify to purchase the median-priced house and make month-to-month funds of $2,304.

That’s near twice the $1,206 month-to-month fee on a median-priced house in 2021, when mortgage charges had been nearer to three p.c and a household incomes $58,000 a 12 months might qualify to purchase a $357,100 house with 20 p.c down.

Jacob Channel

Practically 4 out of 10 Individuals surveyed by LendingTree suppose the housing market is liable to crashing subsequent 12 months, and greater than a 3rd stated they need it to — despite the fact that “a cratering housing market would likely bring down the economy with it,” LendingTree Senior Economist Jacob Channel famous.

Conforming mortgage restrict, 2016-2025

Supply: Federal Housing Finance Company.

Whereas the nationwide median house worth has risen to the purpose the place a giant chunk of renters not incomes six-figure incomes have been priced out of the market, median costs in lots of markets are even larger.

In 2025, mortgage giants Fannie Mae and Freddie Mac shall be allowed to again single-family mortgages of as much as $806,500 in most markets, and loans of as much as $1.2 million in high-cost markets.

Fannie and Freddie’s conforming mortgage restrict, which is tied to house costs, went up for the primary time in a decade in 2017 — a 2 p.c enhance that boosted the restrict by $7,100. After eight extra will increase — together with a record-breaking 18 p.c adjustment in 2022 — the conforming mortgage restrict has practically doubled in lower than a decade.

That’s excellent news for homebuyers who would possibly in any other case should take out jumbo mortgages that may carry larger charges and stricter underwriting necessities than loans backed by Fannie and Freddie. However the dramatic runup within the conforming mortgage restrict is also contributing to larger costs, critics say.

In higher-cost markets, Fannie and Freddie are allowed to buy greater mortgages based mostly on a a number of of the median house worth, as much as a ceiling that’s equal to 150 p.c of the baseline conforming mortgage restrict.

Fannie and Freddie’s 2025 ceiling in high-cost markets shall be $1,209,750 for single-family houses, $1,548,975 for two-unit properties, $1,872,225 for three-unit houses, and $2,326,875 for four-unit properties.

Mortgages backed by the Federal Housing Administration (FHA) are going up as properly, permitting homebuyers placing as little as 3.5 p.c right down to borrow at the least $524,225 in low-cost markets in 2025 and as a lot as $1.2 million in high-cost markets like New York, San Francisco and Washington, D.C.

Costs vs affordability

Whereas the will increase within the uncooked numbers monitoring house worth appreciation are dramatic, they are often deceptive as a result of they don’t consider the influence that rising incomes and fluctuations in mortgage charges can have on affordability.

The First American Actual Home Worth Index (RHPI), which takes these components under consideration, estimated in November that adjusted house costs are nonetheless about 8.5 p.c decrease than the height seen throughout the 2006 housing growth.

However lately, the First American RHPI suggests affordability — or “house-buying power” — declined considerably within the aftermath of the pandemic, because of the run-up in mortgage charges.

Home-buying energy declines

In the course of the pandemic, as family incomes climbed and mortgage charges plummeted to 2.8 p.c, Individuals noticed their house-buying energy climb to a peak of $499,535 in August 2021 as measured by the RHPI.

However by October 2022, as mortgage charges climbed towards 7 p.c, house-buying energy had declined by 33 p.c to $334,791. Home-buying energy has rebounded this 12 months however stays properly under pre-pandemic ranges.

The newest studying of First American’s RHPI confirmed that as of November, the everyday American might afford to purchase a $376,740 home — down 13 p.c from January 2020, the eve of the pandemic — even supposing family earnings rose by practically 24 p.c over that interval, to $84,889.

The distinction? Mortgage charges climbed from a mean of three.6 p.c in January 2020 to six.8 p.c in November 2024.

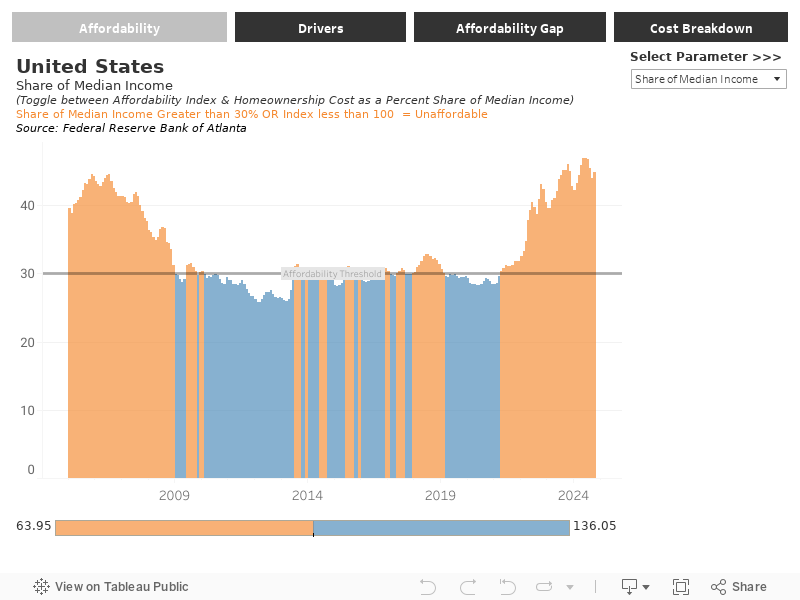

One other means to take a look at affordability is to measure what share of family earnings is required to purchase a median-priced house.

Houses had been final inexpensive in March 2021: HOAM

By that measure, housing affordability is simply as large an issue because it was on the peak of the 2006 housing growth, in keeping with the Federal Reserve Financial institution of Atlanta’s Residence Possession Affordability Monitor (HOAM).

Overlaying the principal and curiosity funds, property taxes and insurance coverage on the median-priced house in October would devour 45 p.c of median family earnings, in keeping with knowledge tracked by HOAM.

Residence purchases that devour greater than 30 p.c of the client’s family earnings are thought of unaffordable by the Division of Housing and City Improvement (HUD).

By that yardstick, the final time houses had been inexpensive was March 2021, when the median house worth was $290,000 and mortgage charges averaged 3.1 p.c.

“It’s potential first-time home buyers that are most challenged, because they don’t have the equity from the sale of an existing home to bring to the closing table,” Kushi stated.

Whereas downpayment help applications will be “very beneficial” for these consumers, “the long-term, sustainable solution to the housing market challenge is more supply,” Kushi stated.

As builders break floor on extra houses — and current owners get extra snug about leaving “ultra-low mortgage rates” behind, Kushi stated — “more supply will allow house prices to gradually come down.”

However affordability “is going to continue to be an issue, given how unaffordable the housing market is, even if you have some positive movement,” Palim stated.

Get Inman’s Mortgage Temporary E-newsletter delivered proper to your inbox. A weekly roundup of all the largest information on the planet of mortgages and closings delivered each Wednesday. Click on right here to subscribe.